I’ve heard I need to wait 2 years after getting a Level 2 General Insurance License before I can take CAIB 4 – is that True?

Absolutely not! Completing your CAIB (Canadian Accredited Insurance Broker) designation and earning a Level 3 General Insurance License are linked by only in a small way.

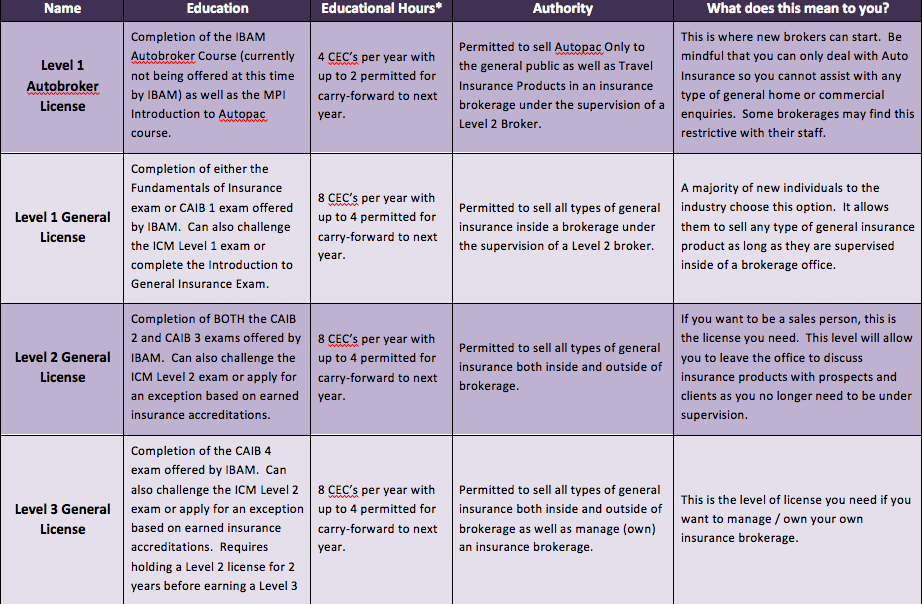

The Insurance Council of Manitoba (ICM) does require that a broker has their Level 2 General Insurance Brokerage for at least 2 years before they can be granted a Level 3 license. This is to help maintain the professionalism of the insurance industry by ensuring that a person has a minimum of 2 years of insurance experience before being granted a license that would permit them to own and manage their own brokerage.

The completion of your CAIB designation can, alternately, be done as quickly or as slowly as you would like. I have seen people complete all 4 exams in under a year which I think is crazy but they were up for the challenge. You will receive your CAIB certificate and can begin using the designation once all 4 exams are successfully passed.

If you do the accelerated method of earning your CAIB’s, ICM will note in their system when you have earned your Level 2 General Insurance License. Once 2 years has passed, because IBAM has already notified them of your successful completion of CAIB 4, your license will be automatically upgraded to a Level 3 license.

So this means… Go for it!! You can always be working towards your designation as education should be a big goal of any insurance broker professional. You just can’t own or manage your own insurance brokerage at this time but there is plenty of time for that – these are the years for you to be learning all you can about the industry.